For example, analysts can calculate the margin per unit sold and use forecast estimates for the upcoming year to calculate the forecasted profit of the company. The concept of contribution margin allows you to compare the relative profitability of two different products, two different services, two different market segments, or two different distribution channels. This concept also offers a means for evaluating the effectiveness of marketing spending and pricing strategies in achieving profit objectives. To figure this out, divide the cost of goods sold for each product by its selling price. For example, if a product costs you $10 to make and you charge $12, your contribution margin is 25%.

Example: contribution margin and target profit

We will find out the break-even point by using the concept of contribution. We will look at how contribution margin equation becomes useful in finding the break-even point. Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos.

- Investors examine contribution margins to determine if a company is using its revenue effectively.

- Our goal is to deliver the most understandable and comprehensive explanations of financial topics using simple writing complemented by helpful graphics and animation videos.

- The contribution margin may also be expressed as fixed costs plus the amount of profit.

- Profits will equal the number of units sold in excess of 3,000 units multiplied by the unit contribution margin.

- The CMR indicates the amount of income a company has left over after all its expenses have been paid.

Create a Free Account and Ask Any Financial Question

On the other hand, contribution margin refers to the difference between revenue and variable costs. At the same time, both measures help analyze a company’s financial performance. In the United States, similar labor-saving processes have been developed, such as the ability to order groceries or fast food online and have it ready when the customer arrives. Do these labor-saving processes change the cost structure for the company?

The Impacts of Fixed and Variable Costs

You can use this information to determine whether your business is profitable or not and whether it is growing or not (if your contribution margin percentage changes). It is essential to understand contribution margins in healthcare because. how do i claim the gi bill for education assistance It gives you an estimate of how much it will cost to run the practice or hospital. It is also used to evaluate if a particular activity or service should be performed at the facility or if it should be outsourced to a third-party provider.

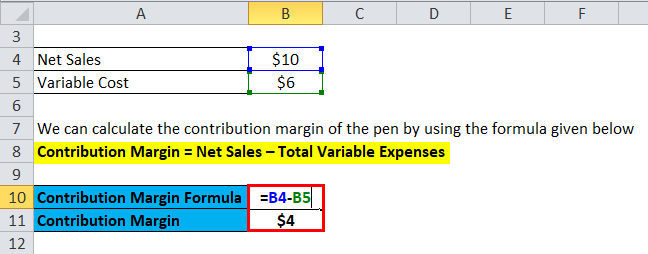

Contribution Margin Formula:

The contribution margin income statement separates the fixed and variables costs on the face of the income statement. This highlights the margin and helps illustrate where a company’s expenses. Variable expenses can be compared year over year to establish a trend and show how profits are affected. The contribution margin measures how efficiently a company can produce products and maintain low levels of variable costs. It is considered a managerial ratio because companies rarely report margins to the public. Instead, management uses this calculation to help improve internal procedures in the production process.

How do you calculate the weighted average contribution margin?

This means not only looking at overall revenue and net profit but also examining the contribution margin of each product or service line. This practice can reveal trends and patterns, helping business owners make proactive adjustments in their operations, pricing, and marketing strategies. This formula reveals the percentage of each sales dollar that remains after variable costs are subtracted. Conceptually, the contribution margin ratio reveals essential information about a manager’s ability to control costs. An important point to be noted here is that fixed costs are not considered while evaluating the contribution margin per unit. As a result, there will be a negative contribution to the contribution margin per unit from the fixed costs component.

For the month of April, sales from the Blue Jay Model contributed \(\$36,000\) toward fixed costs. Looking at contribution margin in total allows managers to evaluate whether a particular product is profitable and how the sales revenue from that product contributes to the overall profitability of the company. In fact, we can create a specialized income statement called a contribution margin income statement to determine how changes in sales volume impact the bottom line. This margin is a critical financial measure for businesses as it helps management make decisions regarding pricing, product mix, and resource allocation based on numbers.

It is important to note that this unit contribution margin can be calculated either in dollars or as a percentage. To demonstrate this principle, let’s consider the costs and revenues of Hicks Manufacturing, a small company that manufactures and sells birdbaths to specialty retailers. Typically, variable costs are only comprised of direct materials, any supplies that would not be consumed if the products were not manufactured, commissions, and piece rate wages.

If a company uses the latest technology, such as online ordering and delivery, this may help the company attract a new type of customer or create loyalty with longstanding customers. In addition, although fixed costs are riskier because they exist regardless of the sales level, once those fixed costs are met, profits grow. All of these new trends result in changes in the composition of fixed and variable costs for a company and it is this composition that helps determine a company’s profit. Consider a small bakery that started analyzing its products using contribution margin analysis. By doing so, the bakery discovered that while its artisan bread had a lower selling price per unit compared to custom cakes, its contribution margin was higher due to lower variable costs. This insight led to a strategic shift in focus towards bread production, enhancing overall profitability.